How to Generate Income During Retirement

Disclaimer: This blog post is general in nature and does not constitute personalised financial advice. We recommend speaking with a financial adviser before making any changes to your investment strategy.

You've spent years building your wealth. But have you thought about what happens when you actually need to use it?

Saving for retirement gets all the airtime. There are calculators, apps, workplace schemes, dinner party debates about KiwiSaver fund types. But the bit that actually matters (the part where you flip the switch from growing your money to living off it) gets surprisingly very little attention.

And yet, it's arguably the trickiest financial transition you'll ever make.

So let's talk about it. How do you actually go from building wealth to generating income from it?

The mindset shift is real

For most of your working life, investing is about accumulation. You put money in, you ride the ups and downs, and you try not to check your balance too often when markets get wobbly. Time is on your side. A bad year? All good! You've got decades to recover.

But when you're drawing down on your portfolio, the rules change. Suddenly, a bad year does matter. You're no longer just watching numbers on a screen. You're relying on those numbers to pay for the groceries, the rates bill, and that trip to see the grandkids in Melbourne.

This shift from "accumulation mode" to "decumulation mode" is one of the biggest psychological adjustments retirees face. And it requires a different strategy.

Five practical ways to make your portfolio work for you

1. Build a small cash buffer

One of the simplest and most effective tools is holding around one to two years' worth of living expenses in cash or near-cash. When markets dip, you can draw from this buffer instead of selling your growth assets at a low point. It buys you time and takes the emotion out of the equation.

2. Adjust your asset mix (but don't go too conservative!)

A common mistake is shifting everything into conservative assets or even cash the moment you retire. It feels safe, but here's the catch. If you're retiring at 65 and could well live to 90 or beyond, that's still a 25+ year investment horizon. You need some growth in your portfolio to keep pace with inflation and avoid running out of money in your later years.

The goal is finding the right balance. Enough stability to weather short-term storms, enough growth to sustain you over the long haul.

3. Be flexible with your withdrawals

The old "4% rule" (where you withdraw 4% of your starting balance each year, hopefully adjusting for inflation) is a useful starting point, but it's a bit rigid for the real world. Markets don't move in straight lines, and neither does life.

And here's something worth saying out loud: it is absolutely okay to spend down your capital. This is your hard-earned money. You saved it to live well. Sure, you might want to leave some behind for the kids, but you can also live alittle. A well-structured plan might see your portfolio gradually decrease over time, and that's not a problem. That's the plan doing exactly what it's supposed to do.

It's also worth thinking about how your spending patterns naturally change through retirement. The early years (your "go-go" years) are often when you're spending the most. You're fit, you're energetic, and you've got a list of places to see and things to do. Travel, hobbies, home renovations, maybe a campervan adventure around the South Island. Later on, spending tends to settle down as life becomes a bit quieter. Your plan should reflect that reality rather than assuming you'll spend the same amount every year for 30 years.

And don't worry too much about withdrawing during a market dip. Yes, it's not ideal to sell at the bottom, but remember, your regular withdrawal is likely just a small portion of your overall portfolio. The rest stays invested and has time to recover. It's not a reason to panic or put your life on hold.

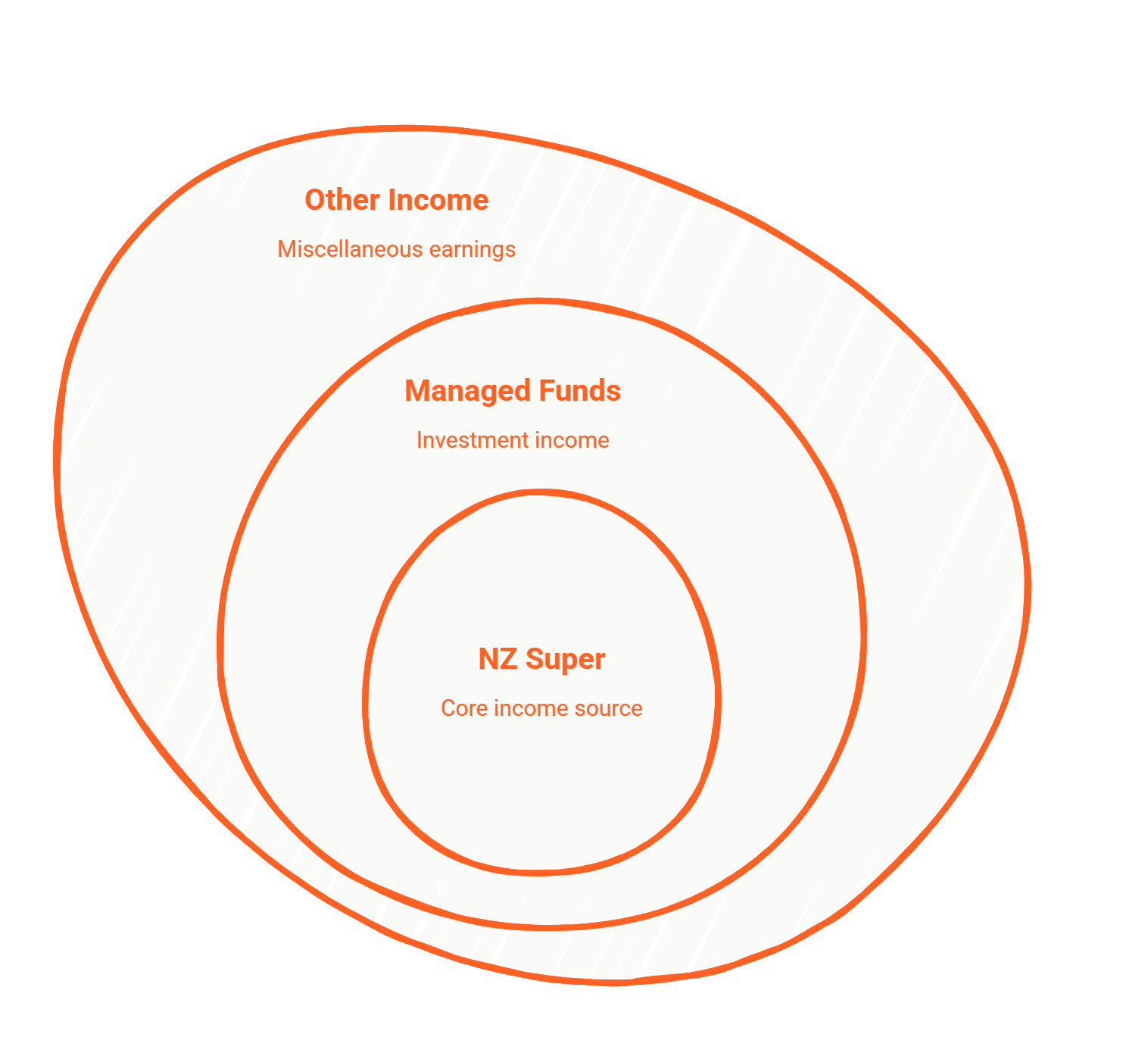

4. Think about income layering

In New Zealand, we're fortunate to have NZ Super as a baseline. But for most people, it's not enough to maintain the lifestyle they want. The key is layering your income sources so you're not overly reliant on any one thing.

That might look something like NZ Super as your foundation, supplemented by income from your managed portfolio, perhaps some rental income, and maybe a part-time gig in the early years if you fancy it. The more diversified your income, the more resilient your retirement.

5. Don't forget about tax

Retirement doesn't mean you stop paying tax (sorry). How you structure your withdrawals can have a meaningful impact on what you actually get to keep. The type of investment entity you're drawing from whether it's a PIE fund, a family trust, or personal holdings, all have different tax treatments.

This is one of those areas where getting proper advice can genuinely save you money. A few smart decisions about where you draw from and when can make a real difference to your after-tax income over the course of a retirement.

The emotional side of spending your savings

Here's something we see all the time with clients. They’ve done a brilliant job saving and investing, but when it comes time to actually spend that money, they freeze up. There's a deep reluctance to watch the balance go down, even when that's exactly what it's there for.

It's completely normal, and it's worth acknowledging. Your portfolio exists to fund your life. Watching it decrease isn't failure, it's the plan working as intended.

A good financial plan gives you the confidence to actually enjoy your money, because you can see in black and white that the numbers work. That you're not going to run out. That you can take that holiday, shout that dinner, help the kids with a deposit, and still be absolutely fine.

So… What next?

Generating income during retirement isn't just about picking a date and flipping a switch. It's about transitioning from one financial strategy to another, from building wealth to making it last.

With some planning, a sensible drawdown strategy, and the right advice, it's entirely manageable.

You've already done the hard work of building the portfolio. Now it's about making sure it does its job for you.

If you'd like to talk through what a retirement income strategy might look like for your situation, we'd love to chat. Get in touch here. The coffee's on us.